The 'Phantom' Menace of ACA Fraud | The Waiting Room

The Trump administration is blaming "phantom enrollees" for 2.6 million Americans losing ACA coverage. The math tells a completely different story.

Charles Gaba is a health care analyst who tracks policy and politics at ACASignups.net. Subscribe to his Substack!

Greetings, Lincoln Square readers!

We’ve agreed to shift The Waiting Room to a monthly format in order to give me more time to put together a more cohesive post instead of a simple “here’s some healthcare stuff which happened the past couple of weeks” bullet list.

That being said, this month I do want to focus on something which happened last Friday afternoon: The Trump Regime’s Health and Human Services Department (HHS) published a new report about enrollment in Affordable Care Act (ACA) individual market exchange healthcare coverage.

There are two main takeaways from this report:

The first is that—as I’ve been predicting since last December—the actual drop in ACA healthcare coverage enrollment was already much higher as of February than the initial, official, Open Enrollment Period (OEP) signup tally had indicated.

While “only” ~1.2 million fewer Americans selected healthcare policies during the 2026 OEP than did in 2025, the actual number with effectuated coverage was 2.6 million lower as of February 2026 (~19.2 million) than in February 2025 (21.8 million). That’s a 12% year over year drop in coverage.

Worse yet, as I’ve also been warning about for months, the more recent effectuated enrollment data available from about a dozen states has shown a continuing decline since February as well, as the folks who were able to come up with the shockingly higher premiums for a few months have been gradually dropping out of their coverage when they’re no longer able to afford it.

The second major takeaway is that—again, as I predicted they would last winter—the Trump Regime, especially via Centers for Medicare & Medicaid Services (CMS) Administrator Dr. Mehmet Oz, is going all in on blaming “waste, fraud & abuse” for the drop in coverage.

The report from the Assistant Secretary for Planning & Evaluation (ASPE) claims that “improper, phantom and fraudulent enrollment peaked at 5.6 million people in 2025.” Since effectuated 2025 enrollment averaged ~22.3 million per month last year, this means they’re claiming that fully 25% of all ACA exchange enrollees were either enrolled “fraudulently” or didn’t exist at all (“phantom enrollees).

Over at The Bulwark, healthcare journalist Jonathan Cohn already tackled the “phantom” nonsense a couple of weeks ago:

TRUMP ADMINISTRATION OFFICIALS have been preparing to explain away declining Affordable Care Act enrollment at least as far back as March, when Oz told NBC News “the fact that we have 23 million makes me think we have too many participants in the ACA—it’s too high of a number.”

The reason, the celebrity doctor claimed, was that millions of enrollees had either lied about their incomes to qualify for big subsidies or had been signed up under false pretenses by unscrupulous brokers and agents. To back up this explanation, officials like Oz frequently cite data showing that a little more than one-third of enrollees filed zero claims last year—proving, they say, that millions of people on the program are there unwittingly, and in some cases illegitimately.

This claim dates back to last year’s debate over whether to extend the subsidies. And it remains as flimsy as it was then. Lots of relatively healthy people don’t file insurance claims in a given twelve-month period. And by design, the Affordable Care Act marketplaces include lots of people getting coverage for just a few months—say, when they are between jobs.

Adjust for that and some other relevant facts, as Brookings Institution economist and former Obama administration official Matthew Fiedler has in a set of calculations, and the percentage of enrollees making no claims lines up nicely with the percentage who do so in employer plans, which nobody would suggest are prone to enrollment fraud.

I actually reformatted Fiedler’s thread into an easier to read format in an earlier post of mine from last fall:

To start, it’s common for insured people to have no claims in a year; not everyone needs care. Is the 35% figure for individual market enrollees unreasonably high, as claimed?

Using the MEPS, I estimate that about 15% of non-elderly people with 12 months of group coverage in 2022 had no medical spending, even though no one thinks phantom enrollees exist in the group market.

And, as others have noted, there’s good reason to expect the individual market rate to be *much* higher: individual market enrollees are typically enrolled for only part of the plan year. Fewer months enrolled mechanically means fewer chances to incur claims.

Concretely, other CMS data show Marketplace enrollment spells averaged only ~8 months in the FFM states in 2024. That’s enough to explain much of the difference between CMS’ estimate of the individual market no-claims rate and my 15% group market estimate.

By Fielder’s calculations, the eight month/year average enrollment period for ACA enrollees would, by itself indicate around 28% of enrollees never filing a claim in a given year:

Here’s the math. Suppose enrollees have a 14.6% chance of generating a claim each month. I’ve chosen this percentage so that if a person was enrolled for 12 months, they’d have a 15% (= [1-0.146]^12) chance of having no claims, matching my group market estimate.

Now suppose that the exact same enrollees were enrolled for only 8 months (the FFM average). In that case, we’d expect 28% (= [1-0.146]^8]) to incur no claims.

There are lots of ways one could refine this calculation, but refinements could actually make the effect of enrollment duration differences larger. What’s clear is that duration matters *a lot*. Plus there could be other big differences between the individual & group markets.

My wife and I have have lived in our current house for 16 years without ever filing a homeowner’s insurance claim. And it’s been over 30 years since I’ve gotten into so much as a fender bender with my car, thankfully … but I’ve dutifully paid my house and auto insurance premiums every month throughout.

As Cohn goes on to note:

To support their argument about fraudulent enrollment, Oz and other officials have drawn heavily on reports by the Paragon Health Institute, a right-leaning think tank, which argue that the Biden administration’s efforts to grease the wheels for enrollment enabled fraud on a mass scale.

… Nobody disputes that the Affordable Care Act marketplaces attracted some agents and brokers who enrolled people using unethical, possibly illegal methods—like signing up people or switching their plans without permission—to get commissions … But the scale of that problem is what’s in dispute. The estimate in a recent Paragon report that there are more than 6 million improper or fraudulent enrollees rests on some assumptions that are highly contestable—and, in fact, have been strenuously contested.

Yes, that’s right: They double-counted anyone who switched policies partway through the year.

Millions of people who moved, got married or divorced, gave birth or adopted a child, turned 26 and had to leave their parents policy for their own, etc. were counted twice if they didn’t happen to visit the doctor during the few months they were enrolled in either policy (which is actually pretty frequent for young adults, I should note…it’s a royal pain in the ass getting my college kid just to visit the doctor for his annual checkup).

Fiedler also points out that even if there were a significant number of “phantom enrollees,” thanks to the ACA’s Medical Loss Ratio (MLR) rule which requires insurance carriers to spend at least 80% of premium revenue on actual medical claims, eliminating them wouldn’t actually save the federal government money, since that would just mean that the carriers would be spreading their overhead out over fewer enrollees.

After all, an enrollee who never visits the doctor is an enrollee who never files a claim, which means that the cost of treating enrollees who do file claims would be higher to the carriers on a per-enrollee basis…which in turn would mean the government would still be paying out roughly the same amount in subsidies to cover the higher premiums which would follow.

The ASPE report also makes other claims which include a few which were legitimate a couple of years back (in particular, the broker fraud scandal story first reported on by Julie Appleby of KFF Health News back in 2024)…but which also include several which are based on either tortured or circular logic.

For example, it claims that:

“Trump Administration program integrity efforts stopped about 1.5 million enrollees from receiving subsidies they did not qualify for and ended or blocked another 1.4 million through February 2026, for a total of 2.9 million people who had previously been improperly receiving subsidies they did not qualify for.”

And how did they do that exactly? Well, later in the report it says:

We estimate another 1.4 million have either been removed or blocked from enrollment due to additional program integrity measures such as ending the year-round enrollment period for people with incomes between 100 and 150 percent of FPL.

Yes, that’s right: They “removed or blocked” 1.4 million people from enrolling by no longer allowing low-income Americans to enroll year-round. Claiming that this “prevents fraudulent enrollment” is like a public pool preventing people from drowning by filling the pool in with cement.

If you read through the 12-page report (plus 4 pages of citations), you’ll notice that the words “potential,” “potentially” or “suspected” appear no fewer than 13 times:

Potentially large-scale improper, phantom, and fraudulent participation has been

reduced, but not fully resolved…

Removing Eligibility Verifications Enabled Potential Abuse of $0 Premium Plans

Figure 2 highlights the potential fraud by showing a spike in zero claiming among low-income enrollees after 2020

… vulnerabilities potentially leading to improper and fraudulent enrollment

… there remains 2.6 million potentially improper or fraudulent enrollees in 2026

… the ACA Exchanges experienced unprecedented enrollment growth from 2021 to 2024, nearly half of which was suspected to be improper, phantom, or fraudulent.

… suspected improper, phantom, and fraudulent enrollment resulting from recent federal policies

High Levels of Suspected Improper and Fraudulent Enrollments

… significant increase in suspected improper, phantom, or fraudulent enrollment in ACA Exchange plan

… Beyond fiscal integrity concerns associated with suspected fraudulent or improper enrollees could incur surprise tax liabilities

… Looking at enrollment figures alone lacks critical context surrounding the suspected levels of improper and fraudulent enrollment

… new regulations to improve program integrity, investigating suspected improper or fraudulent enrollment

I’m sorry, but “suspecting” someone of “potential” fraud isn’t the same thing as having actual evidence of fraud.

Again: Yes, the broker fraud scandal was real…but it was mostly cracked down on by the Biden Administration in their final months in office and has presumably been dealt with even more severely by the Trump Regime over the past year or so. Last fall, in fact, one of the proposed compromise bills to extend the enhanced federal subsidies which expired back in December included a bipartisan provision which would have included:

… new guardrails to prevent “ghost beneficiaries,” crack down on fraud, and enhance delivery clarity. The bill cracks down on broker fraud by implementing several measures, including those presented in the Insurance Fraud Accountability Act, to codify CMS’s authority to remove bad actors from ACA marketplaces, penalize bad actors, implement new consumer protections, and more. It also directs ACA marketplaces to regularly confirm enrollee eligibility with the Death Master File and requires marketplaces to better notify recipients the value of PTCs they are receiving from the federal government.

… all of which would have been perfectly fine with congressional Democrats, frankly … but in the end congressional Republicans refused to let the bill even get a vote.

Most of the rest of the claims of “fraud” or “phantom enrollees,” meanwhile, appear to be either phantoms themselves or vastly overstated…and again, as far as I can tell it’s unscrupulous brokers who seem to be at fault, not the actual enrollees themselves in the vast majority of cases anyway. If the Trump Regime has proof of millions of enrollees committing fraud, where are the indictments? Where are the arrests?

The report claims that there are “1 million highly suspicious agent and broker assisted enrollments through Healthcare.gov with no social security number on their application who are also paying no premium.”

…except that last year there were around 1.4 million lawfully present immigrants legally enrolled, many of whom presumably don’t have social security numbers because, by definition, they aren’t U.S. citizens, and only certain categories of non-citizens can have SSNs in the first place.

Regarding immigrants applying for ACA coverage & subsidies, via the Center on Budget & Policy Priorities (CBPP):

… Individuals applying for premium tax credits for their dependents or spouse and not for themselves only need to provide their SSN if: (1) they have an SSN, and (2) they filed a tax return for the year for which tax data would be used to verify their household income and family size. The ACA marketplaces use SSNs to conduct data matches with the Social Security Administration (SSA) and the Internal Revenue Service (IRS). When these matches can successfully verify key information like income, people may not have to submit proof of their circumstances.

… Someone who uses an Individual Taxpayer Identification Number (ITIN) to file taxes is not required to provide an SSN on the application and should skip the question in the application. (The application will make multiple requests for the SSN. Each time the person should skip it.)

Did these folks have an ITIN instead? The ASPE report doesn’t say one way or the other.

As it happens, one of the largest categories of non-citizens who were eligible for ACA subsidies (around 237,000 enrollees last year) happened to be documented immigrants who earn less than 138% of the Federal Poverty Level but who aren’t eligible for Medicaid due to having lived in the U.S. for less than five years. By definition, these folks would have been eligible for $0-premium plans … right up until Republicans allowed the enhanced subsidies to expire, that is.

The report also states that they “removed another 200,000 people from subsidies for failing to file and reconcile taxes for two consecutive years.” Yes, that’s true … but that’s because they changed the requirement, which had been two consecutive years under the Biden Administration to one year under the Trump Regime. That doesn’t mean that those 200,000 people were “improperly enrolled” at the time.

Frankly, the main “evidence” of “millions of people” being “fraudulently enrolled” seems to be the fact that they lost coverage in & of itself.

I’m reminded of a panel from “Munro,” the short comic story by Jules Feiffer in which a 4-year old boy is accidentally drafted into the army. When he points out to the sergeant that he’s only 4 years old, the sergeant responds: “It is the official policy of the Army not to draft men of four. Ergo you cannot be four. Ergo you only think you are four. Go on sick call.”

This is exactly what I and other healthcare policy wonks have been expecting, and it’s typical of Trump Regime “logic:”

If they kill a random Venezuelan fisherman via an airstrike, that “proves” they were a drug dealer by definition.

If someone loses healthcare coverage due to Trump Regime policies, it “proves” they were enrolled fraudulently by definition.

(Sigh) in any event, I expect the Trump Regime to continue to push the “fraud/ phantom enrollee” excuse even harder as the coverage numbers continue to drop.

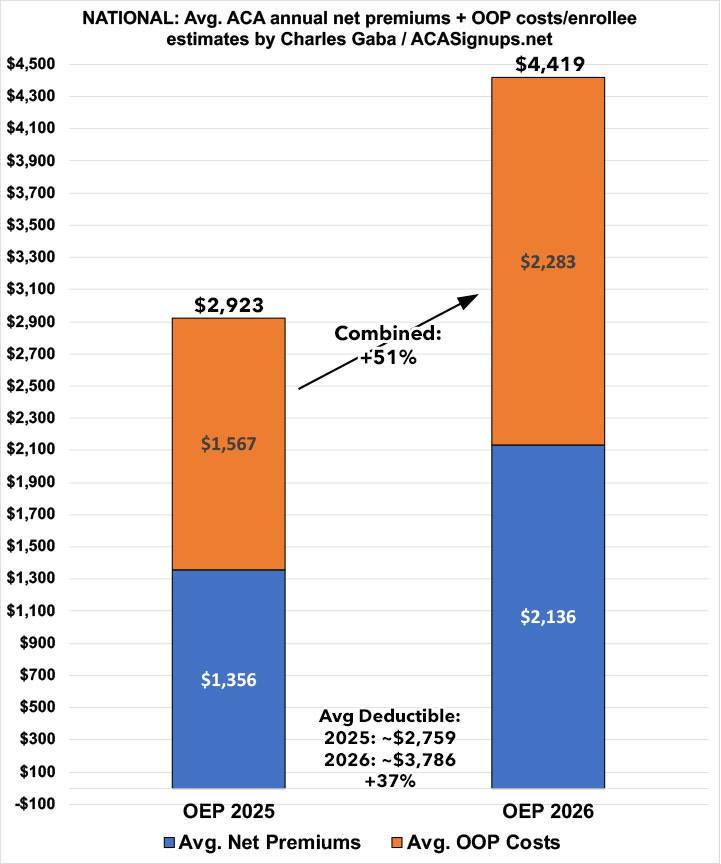

Speaking of which, that brings me to the other major story I’ve been working on for the past several weeks: My state-by-state cost analysis of just how much premiums and out of pocket expenses have jumped this year on average for the ~19.2 million Americans who weren’t completely priced out of the market altogether during Open Enrollment.

I discussed this in the last issue back in late May, but as a refresher:

… The other big shoe which is dropping this year is increased out of pocket costs as millions of the ~19.2 million or so remaining enrollees…have been forced to downgrade their coverage to avoid (or at least minimize) those massive premium spikes.

In most cases this means moving to plans with higher deductibles, higher co-pays and higher coinsurance costs. In many cases this has also included moving to plasn with worse networks, referral requirements to see specialists and so on.

… Average net premiums are easy to calculate, since the Centers for Medicare & Medicaid Services (CMS) has already published Public Use Files including the average gross and net premiums which all ~23.1 million people who selected exchange coverage during the Open Enrollment Period (OEP) are being charged.

… Out of pocket expenses are a lot trickier, but I’ve come up with a formula which seems to be fairly accurate. It gets wonky, and you can see the full methodology here, but it basically boils down to a) calculating the average Actuarial Value (AV) of the entire ACA market within each state and then b) using that AV to estimate total average medical expenses in both 2025 and 2026.

As of this writing, I’ve completed 46 states and D.C. (up through Virginia) with four states left to go. You can read the analysis for each state by reviewing my official Substack feed over the past month or so…or you can use the drop-down menu over at ACASignups.net to pick a state, any state.

Nationally, however, on average (and with several important caveats, especially regarding the out of pocket expenses), ACA enrollees are paying around ~$780 more in premiums and ~$700 more in out of pocket expenses (deductibles, co-pays, etc) apiece than they did last year … around $1,500 more or roughly a 51% increase in net healthcare costs.

And yes, the vast bulk of this is due directly to congressional Republicans allowing the enhanced tax credits to expire (along with other administrative changes made by the Trump Regime).

See you in August…

It should be noted that another number that’s being explained away or discounted is the number of us who have been forced to lower our coverage from “gold” to “bronze” plans. We’re small business owners, we’ve always been income ineligible for premium tax credits, we buy our health insurance through the ACA marketplace because we have no other options to buy health insurance because we’re required to buy through the ACA marketplace. We are now paying $1800/mo for our bronze plan with a $28,000 family deductible, and then, after meeting that deductible, it covers 80% coverage of “allowable charges for pre-approved treatment with in-network providers.” We do not have coverage for prescriptions, vision, dental, or any other “non-medical”services. Our “gold” coverage went up to $2400/mo for the same coverage at open enrollment, again as small business owners who have always been income ineligible for premium tax credits. This is for the two of us as we can no longer afford to cover our college age kids. At these rates and coverage we will most likely not continue to purchase health insurance coverage next year. For-profit health insurance is simply non-sustainable for much of the American population who are self-employed, income ineligible for premium tax credits, and have no other options than to purchase health insurance through the ACA Marketplace. The same ACA Marketplace that first gave us those options as small business owners years ago when we had no other options.

I am slightly off topic here, but In my opinion the vast majority of the fraud in insurance including medicare is big players upcoding procedures so they can get more money out of the system. As a stupid idea, just to explain, the doctor uses a tongue depressor to look at your throat for 5 seconds and codes it as a complex examination for possible throat cancer. For us "we the people" I am sure there is some fraud but it is tiny in comparison